Let Me Explain...

A special sit with estimated +29.4% return.

Every investor, at some point, looks around and thinks:

’What the hell am I supposed to buy now?’

You’ve probably had that moment more than once as well.

It’s weird out there. AI stocks are trading at 30x sales, IPOs are doubling on day one, and companies with no profits (and sometimes no revenue) are getting billion-dollar valuations. Everything’s priced like the ‘good times’ will never end.

And if you’re a value investor? You feel it even more. The obvious bargains that appeared after the COVID correction in 2020 are, for the most part, long gone. The stuff that is cheap usually has a reason for it now. And the businesses you do like? They’re usually priced for perfection, leaving zero room for mistakes - and buying stuff without a margin of safety is a big no-no for any respectable investor.

Meanwhile, everyone and their dog is starting a Substack, writing about the latest trends - AI, semiconductors, whatever happens to be the hottest, or the so called ‘hidden gems’, stocks that for some unknown reason everyone just ignores! (which just coincidentally often happen to be cyclicals at the peak of the market cycle.)

There’s no shortage of opinions, I assure you. But real, compelling opportunities? They’re getting a lot harder to find nowadays.

So, what should you do? Sit in cash and hope for a market crash? Or maybe give in and start chasing the momentum trying to get lucky?

Neither of those sound like a great plan.

But there’s another way - one that’s worked before, in markets just like this.

It’s what Buffett did when he ran his partnership. Whenever the market got too hot, when traditional value plays were scarce, when he needed a strategy that wasn’t tied to the market’s every move, he leaned into special situations.

So, what do I do when the market is this expensive?

I take a page out of Buffett’s old playbook.

Why Special Sits?

When markets become expensive, traditional value opportunities dry up, forcing investors to look elsewhere for good returns. Special situations - such as liquidations, mergers, restructurings, or spin-offs - offer a way to invest in opportunities where returns are driven by a specific corporate action rather than overall market trends.

If you’re into special situations, You Can Be a Stock Market Genius by Joel Greenblatt is an absoulte must-read. I know, I know - the title sounds like something your uncle who just discovered day trading would recommend right before blowing up his account. But trust me, it’s a classic. Greenblatt lays out how to find great opportunities in a way that’s actually fun to read (which is saying something for a book about stocks). If you haven’t picked it up yet, do it. Worst case? You don’t become a genius, but at least you’ll have a better excuse for bad stock picks…

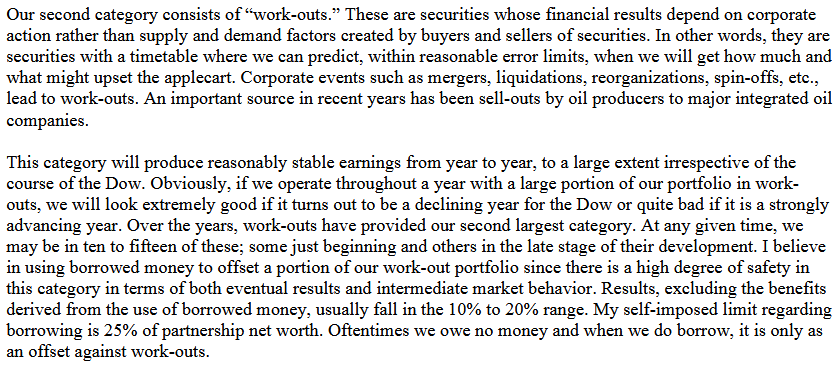

Warren Buffett frequently used this approach in his early years when he thought the market was getting too hot, focusing on what he called “workouts”.

Definitely not something I usually look at.

I usually skip biotech stocks. I don’t screen for them, I don’t read any writeups on them, I don’t follow any people on Twitter that specialize in that kind of stuff. It’s either too complex for my limited brain that only knows how to analyze cigar-butts, or just feels too risky overall.

Most of them follow the same script - hype up a breakthrough drug and burn through cash keeping the dream alive just long enough to string investors along. Then comes the clinical trial flop, the stock tanks 90%, and everyone left holding shares is stuck wondering what the hell just happened.

But every once in a while, one of these train wrecks turns into something way more interesting.

This one company just pulled the plug on its lead program, slashed over 80% of its workforce, and kicked off a strategic review - which here means one thing:

A special sit opportunity in the making.

Am I that bold to say that Buffett would be buying busted biopharma stocks if he were young again today?

I don’t know, maybe I am. But let’s be real - the man had a whole menu of cheap net-nets, sleepy insurance companies, and other 1960s financial relics trading at 1/4th of liquidation value to pick from, and investing isn’t about time travel - it’s about making money with what’s in front of you.

But right now? The risk/reward here looks pretty damn good.

So yeah, maybe. Or maybe I’m an idiot.

Normally, I wouldn’t bother. But with the company now trading well below net cash, high insider ownership and executives suddenly lining up change-in-control bonuses, it was hard to ignore.

And before you think I’ve gone crazy with today’s stock…