Fear and Loathing in Orchard Funding Group

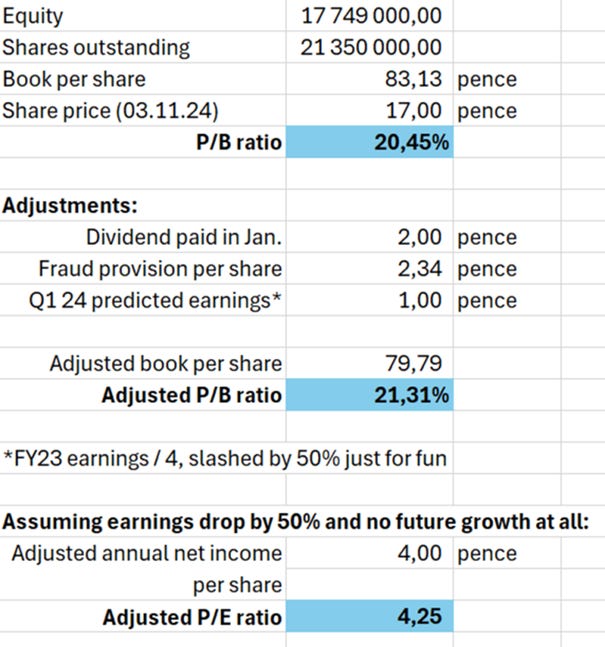

Orchard Funding Group (ORCH.L) is trading for 20% of book value and ~2 P/E, based on FY 2023 results, and an 18% dividend yield.

05/06/2024 Update:

The investment was very successful for me and for many others, I suppose! For people that bought at the very bottom there was an ~85% return in just a single month. I’m still holding Orchard (5% allocation), but now it’s more of a tender play, which I think might still be a lucrative way of using spare cash. I also decided it’s a good moment to take down the paywall and make this article free for all to read.

09/04/2024 Update:

The latest half year results have been released. This slightly changes the thesis here, as a potential tender offer/share buybacks have been announced, as well as Ravi disclosing potentially buying shares on the market, thus setting a price floor for the investors in case of a take private. The price increased to around 21p, which still looks extremely cheap.

Everything is going pretty much where I thought it would.

TL;DR:

ORCH is trading for 20% of book and 2 last year’s P/E. There’s not much wrong with the company, but the CEO is hated by the shareholders for not being responsive. Most of the long-term shareholders have already sold out after the company recently got hit with some operational problems, driving the price down to ridiculous levels. There are also talks of a delisting/take-private, which is considered to be a risk factor by the old, angry shareholders, but turns out to be far-fetched after looking at the dry facts. The investment has a wide margin of safety, but the overwhelmingly negative sentiment of the former shareholders, as well as the lack of interest from new investors caused the company to trade at an irrationally inefficient price.

Summary

Orchard Funding Group is a £3.5m market cap company listed on AIM, which through its wholly owned subsidiaries specializes in insurance premium finance, professional fee funding and financing for other service fees.

It’s inefficiently priced at around 20% of book value and ~2 P/E, based on FY 2023 results. Last year it paid a dividend of 3 pence per share, which calculates to around 18% dividend yield, based on the closing price of 17 pence per share at the time of writing this article. Since its IPO in 2015, the company had not had any unprofitable years, including 2020 and thereafter, when the pandemic hit. The CEO currently owns 54% of the company and has been managing it since first starting it in 2002, when he created Bexhill, currently one of the Group’s subsidiaries.

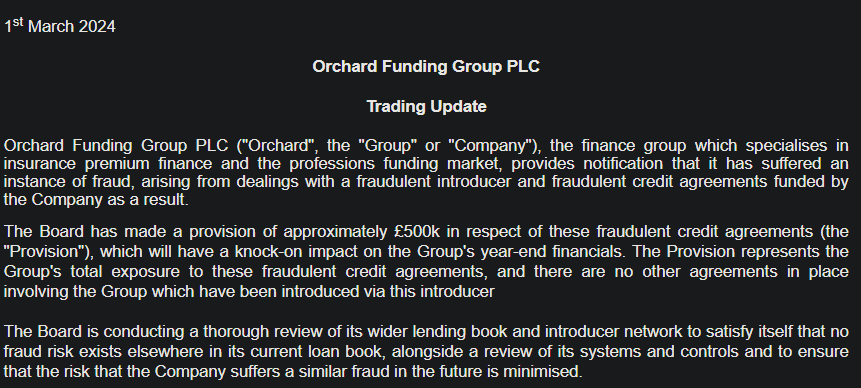

In the beginning of February, the company had been hit with news of potential GAP (guaranteed asset protection) insurance ban in the UK which, at this moment, accounts for around 20% of total assets of the company, as well as an instance of fraud worth approximately £500k.

Source: Trading Update as of 02/02/2024

Source: Trading Update as of 01/03/2024

Those events caused the stock price to fall over 50%, from £0.37 to £0.17 YTD.

In my view, that was an extreme overreaction, and now Orchard is trading at a dirt cheap price, with a wide tangible margin of safety.

*Note that this is a very illiquid stock. Average volume is around 70k shares daily, which is around $12k a day, so this one is mostly for smaller accounts and private investors. There are days when there’s no liquidity at all. Buyer beware!

Valuation

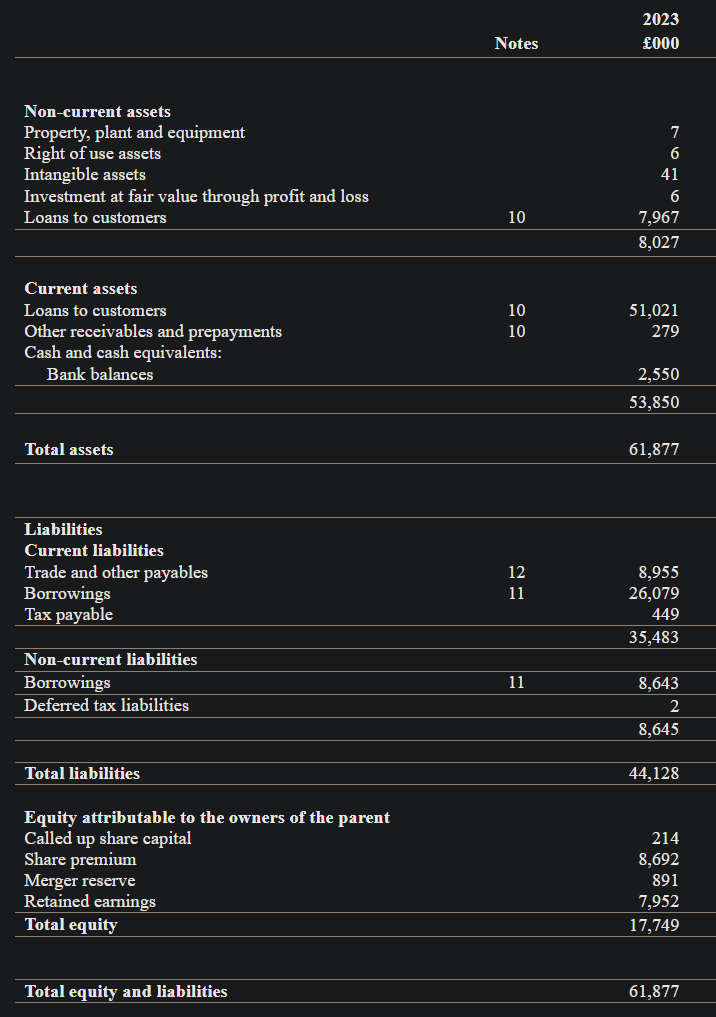

Source: FY2023 Annual Report

Book value adjusted for the aforementioned things seems to hover around 20%. All of this is cash in a form of loans to customers, mind you.

If we assume that the recent issues with GAP insurance cause the company to lose half of its annual earnings and, adding no future growth at all on top of that, it looks like the adjusted P/E ratio is 4.25.

Source: my own calculations

The GAP insurance is said to use around 20% of total assets. Most of the assets belong to the Standard lending segment, with a much smaller amount belonging to the Toyota products segment, which is said to be riskless, but also much less profitable.

Source: FY2023 Annual Report

This 20% of total assets amounts to around £12.5M. This amount is the money that’ll have to be put to work elsewhere, assuming the “ban” remains. GAP insurance is written for approx. 3 years. Assuming the current loans all finish their lifetime together in those 3 years, this means that for the next 3 years the earnings recently seen should not radically decrease.

Our 4.25 P/E (assuming this 50% reduction in earnings from day one, from now on and forever, with no future growth included) may then turn out to be too conservative.

04/09/2024 Update

It was confirmed in the latest report that the current loans should be bringing cash for the next 3 years, as mentioned above, with no impairments.

To clarify, as per Investopedia:

“Gap insurance is a type of auto insurance that you can purchase to protect yourself in case you total your car and the amount of compensation you receive does not fully cover the amount you owe on your financing or lease agreement.

I will not get deep into the controversies of GAP insurance, nor will I try to predict the future earnings of Orchard, as a) in my view rough calculations like those above definitely suffice, and b) it is practically impossible to predict politics. One thing I will mention though is that most of the high commission that the UK regulators don’t like so much is earned by the dealers, not the insurance companies themselves. This “ban” can as well turn out to just be temporary, as it does not seem like the best way to protect the car buyers from paying high prices for insurance is to completely get rid of the insurance, but of course it may as well turn out to be worse than I think.

Source: InsuranceBusinessMag

Lending results

Source: FY2023 Annual Report

Source: FY2020 Annual Report

As you can see the results for the past few years were stable. Even the pandemic crisis did not really hurt the company that much, as to be overly concerned with potential recessionary performance (assuming its current share price of 17 pence, that is) It did get hit with some temporary headwinds, but it looks like even considering the inflation caused by the pandemic, Orchard is and should continue to be steadily growing. This is mostly due to the fact that the type of lending Orchard does is not very cyclical, and the underwriting seems to be of fairly high quality. The average return on equity is around 10%, which is quite good for an insurance company. From its IPO, Orchard has seen steadily increasing revenue and loan volume every year (apart from the times of the COVID-19 crisis, that is). One question I could not exactly solve at first (from the standpoint of their operations) is why then since the IPO the share price has been steadily decreasing:

There’s a reason for the chart to be looking like that, but I’ll talk about that later.

Some other notable things

Orchard is really small:

The management likes to emphasize the quality of its lending practices:

Source: FY2023 Annual Report

The company has recently issued a bond. Its price did not necessarily react as heavily to the recent events as common shares did:

Source: www.hl.co.uk

Of course, that may also be due to the tiny size of the market for that bond, but I suppose that if the bondholders sensed some huge danger as a result of those unfavorable events, they would without a doubt try to get out, driving the price down.

No matter how you look at the case, ORCH looks cheap. This inefficiency may correct itself very soon, as there seem not to be any good reasons for the shares to be priced this way. There are risks, of course, but nothing that would justify this current valuation. The company looks like it’s operating in a conservative way, with large tangible margin of safety on top of that for the common stock investors. Thus, the risk of permanent loss of capital seems to be minimal in this case. The CEO owns over half of the company, and the management overall seems to be shareholder friendly. Seriously, just read the recent annual report. Although it’s difficult to predict anything here, the rerating should happen when the market participants realize how absurd the current price is. I could not understand why someone would sell shares to me at such a low price. I tried to find some explanation for this, and figure out who was on the other side this whole time.

And then I finally found the skeletons in the closet…

All of this looked perfect until I texted one former shareholder of Orchard. And then another one, and another one.

This is where it gets interesting, but also REALLY complex at first. I’ll try to explain everything to you chronologically, the same way my thoughts were evolving.

The shareholders

I decided to text one former large shareholder of ORCH and ask about his opinion on what is going on. I noticed that he was actually selling his shares quite quickly recently (as seen in the recent Trading Updates posted on the company’s website) and wanted to understand why. He said that Ravi, the CEO, should not be trusted. This guy had been with the company for a long time and mentioned that Ravi was a really unfriendly person, and there were a lot of communication problems between him and the rest of the shareholders. That the long-time shareholders were very unsatisfied with the lack of clear communication and how he treated them. Did not care about improving the share price at all, did not disclose much information, unless he really had to. He treated the company as if it were private.

Then that former shareholder said that Ravi is probably planning to delist and that my money’s going to be frozen, so I better watch out. I had a sizeable position in ORCH at that time and, understandably, I became frightened that I made a big mistake.

Then I texted another former shareholder and he basically told me the same things, but in a different way. He mentioned the risk of delisting and pretty much having my money frozen. Nonetheless, before deciding what to do with my shares I thought I’d be prudent to confirm the facts myself first.

I won’t post any screenshots or disclose the identities of those people, but one of them sent me a link to a chat where ORCH shareholders have been exchanging their thoughts on the company. Just read that and you’ll understand how the sentiment looks like.

I thought to myself, let’s calculate the odds, without any emotions. Just pure facts. Talking to those guys changed a lot in the thesis. Suddenly there appeared to be a lot of unpleasant ways for me to lose money on the investment I have not taken into consideration before.

The process

Let’s consider Ravi, the CEO, is as evil as they describe him. He’s the devil and he wants to screw the shareholders for his own benefit. What are his options?

Option 1:

Well, the first one is the delisting, as the first shareholder mentioned. Many investors would be sure to lose a lot of money, as after a delisting gets announced, the share price falls as to account for all of the people that don’t want to hold shares that they cannot later sell. That is scary.

But what would be the pros of this for Ravi?

- Reduced costs, as being a listed company costs money, quite a lot of it for such a small company actually.

- He can try to come back later and “start all over” with being a publicly traded company.

What are the cons of this for Ravi?

- Losing access to a public market where he can buy cheap shares and sell them later at a profit. That’s a big one.

- More pissed off minority shareholders.

- Potential lawsuits.

- Probably increased debt costs – a public company is heavily regulated and can have lower cost of debt than a private one, as banks factor that as something that lowers the risk. More credibility, less riskiness.

Additionally, and that is also a big one, he’d need 75% of the votes to delist the company (UK law requires 75% of the votes for delisting to happen)

He himself, together with his family owns maybe 60%, so he’d need the 15% from somewhere. One place he could get the shares from is Gresham House Asset Management, another large shareholder. They own something around that. One of the shareholders I talked to mentioned that Ravi is actually discussing that with Gresham, trying to get them to sell their shares, as he heard that from one of the portfolio managers working there. So, if they sell, Ravi can easily delist.

But why would he do that? The “evil and greedy Ravi” can definitely do something else to earn more cash for himself at the expense of the shareholders.

04/09/2024 Update

It was confirmed that they’ll probably be looking for a delisting coupled with capital return measures. I am not sure if by share cancellation they mean a pure delisting or a buyout delisting. For the first thing to happen the same rules as those mentioned above apply – 75% of the votes (so probably a tender at a premium, or a buyback at the current prices, or both, for Ravi to reach that 75%), minimum price floor in case Ravi buys more shares for himself to take the company private later. Also, there was a “partial exit” for the current shareholders mentioned. So maybe the minority will get bought out? That’s difficult to say at the moment.

Let’s consider option 2, taking the company private.

What would be the pros of this for Ravi?

- He buys the company at an extremely cheap price, thus getting a fantastic return on investment.

- He does not have to deal with annoying shareholders anymore.

- He can do an IPO later to return to Orchard being a publicly traded company and start all over

What are the cons of this for Ravi?

- Higher cost of debt, probably

He’d also need 75% of the votes in this case. So, with that in mind, 2 things can happen:

Gresham sells, or Ravi gets his 75% some other way. Remember, to do anything of this sort he has to buy more shares to get the 75% or make us a voluntary offer for a buyout that the current shareholders don’t necessarily have to accept. First, read this:

It basically means that "if Ravi wants the offer, he'll have to buy more shares from, for example, Gresham, effectively locking in the minimum price". Gresham, if at all, definitely won't sell BELOW the current share price, probably even demanding a premium, and if they even sell at the current market price (say, 17p), that's going to be the price floor, the margin of safety for us here in case of a buyout from Ravi. He won’t be able to give us less than that. Additionally, Gresham will probably not want to sell at all, as the shares they hold are intrinsically worth a lot more than what they're trading for now, and they know it.

Gresham does not sell and Ravi can’t get the 75% for a buyout, so it’s either the voluntary offer (which should not get accepted as a whole, without a sufficient price premium, if Ravi wouldn’t find any individual sellers previously in this case) or just business as usual (so for investors with an average of, say, 17p, it’s all sunshine and flowers. Maybe Ravi tries to buy shares on the market, but again, price floor for us then.

So, pure delisting makes little sense, but of course is a possibility, but taking the company private at a bargain price makes a lot of sense. What now?

In case of a take-private, a voluntary offer makes less sense than a forced mandatory one, as for the shareholders to accept it, the buyout price would have to be a lot higher than the current market price (another part of the margin of safety, one would not lose money in this case). There is the risk of the deal not being accepted, and Ravi getting nothing, so he cannot simply try to buy it all for 10p when it’s trading at 17p. A surer way of maximizing profits is forcing the shareholders to sell their shares to Ravi at the lowest price possible to get the 75% of votes.

In order to get that he’d need to buy them from someone. Again, buying any shares on an open market would set the minimum buyout price for Ravi. So, if the price stays at 17p, this is the price floor for the investors. The only risk of losing money would be for the company to go down even more for some reason, and only then being offered a lower buyout price by Ravi.

You see where this is going?

The old shareholders were extremely angry, emotional selling led to the share price falling to an irrational level. I tried to convince those I talked to that at 17p this might be a great opportunity and Ravi can’t hurt them more without hurting himself this time, but they wouldn’t even listen. Most of them didn’t want to even consider going back. The sentiment was as low as could get.

The “delist-and-lose-all” fears were mostly irrational, as just by looking at plain facts one could easily understand that the downside is heavily protected, but the shareholders were few and far between, and most of them were just so upset that they could not think straight. That was just a perfect storm for them, and an opportunity for those few of us who came in with fresh thinking.

Continuing

So purely delisting was one option, but it was not that reasonable. Take-private was the second one, but that would probably leave us with a price floor either way, so there was little risk for us to lose money, even if the buyout offer’s price was set really low. In a bad scenario investors would not lose much (if at all) but could gain a lot. The third option was that none of that would happen and ORCH would remain a public company, but I’m not even considering this one as it’d be all sunshine and flowers if that was the case. What I wanted to know is how I can lose money here.

It turned out there are actually ways to lose money. Here’s a list of most of them:

- Gresham (or other large holders for this matter) does not sell at 17p, but the price falls further and they sell lower, the company gets bought by Ravi for even cheaper than 17p, and we permanently lose a part our invested capital. For that to happen, people responsible for this investment at Gresham would need to either get emotionally tired or desperate. After all, why would they sell at such a ridiculous valuation? They have a fine company trading for less than 20% of book value and something like 2-4 P/E. Irrationality would have to be the reason for them to dispose of the shares. Or maybe liquidity problems.

- Ravi actually starts threatening the shareholders by saying: “here’s a tender for 15p, if you don’t sell, you’ll be holding shares you cannot sell after we delist later”. Reputational risk for him, no doubt about that, but could still happen. Anyways, I’d be glad to hold shares in a delisted company earning half of its market cap annually and paying out an 18% dividend. The only loss would be for those who sold in this case. After the recent half year update and this whole “partial exit and share cancellation” the odds increased for this one, but again, if you’re fine with holding shares like that then you shouldn’t worry.

- Nothing of this sort happens and the business just continues as usual, but the company gets into some operational trouble and the earnings degrade drastically. So just normal operational risks. Something huge would have to happen though, like a large fraud case, as the tangible margin of safety is just enormous, so investors are well protected.

- Ravi starts buying shares to get the desired 75% and after he reaches that, he stops for 12 months, after which the price floor gets a reset. Then he can offer us a low price, forcing us to sell. I’m not entirely sure about the legal side of this though, so that’d have to be confirmed.

- Another thing might just be that Ravi does not have the means to take the company private himself, but I would not think of that as a high-probability case, as the company’s market cap is just so tiny, and spending a few hundred thousand more to reach that 75% threshold does not seem like a big deal for him.

Last few words

This whole “evil Ravi” thing is pretty far-fetched too, in my view. I don’t think Ravi is necessarily an evil person, or does not care about the shareholders at all. Fine, maybe there were problems with communication between the company and the shareholders, but frankly that was the only real concern those guys I talked to had. There were no scams, nothing illegal, just purely bad communication. And as those guys got really involved personally with the investment they slowly became more and more mad at the CEO after not being listened to. It’s fair to say that Ravi treats the company as if it were his own private enterprise, that’s true, as well as the fact that the relations with the investors can definitely be improved, but I do not think that these things justify the current price. This looks like a complex and difficult to understand case at first, but in fact it is really simple intrinsically. All you need to look at is the incentives and the rest takes care of itself. And it’s not like it’s a riskless arbitrage, a sure thing, but it surely deserve some new, fresh investors to take a look at, consider the prevailing irrationality, and maybe use that for their advantage. After all, even if my shares get delisted, in the worst case scenario, I’d still be holding shares in a stable company I bought for 20% book and a P/E ratio in low single digits.

I might have missed some things, so if you have any thoughts on anything here be sure to let me know! I’m more than happy to discuss this case anytime!

Fascinating story. If I had read this at the time, I probably would have been to wary to put money into this though. The illiquidity + management that probably does not have my best interest at heart would have scared me off. Glad it worked for you!

what is the current situation and attractiveness?